I recently wrote an article about the practical considerations that should be made prior to dropping everything in order to pursue a professional life of “doing what you love,” whatever that may mean.

I encouraged people to consider things like how many “favours” their business will need to survive, how many hours they are actually willing to allocate towards their passion before it starts feeling like a chore, and how prepared they are to be broke. On a final note, I urged everyone to consider the implications of eventually having dependents, be it personally or professionally, wholly or partially.

It is there where I’d like to pick up and close out the conversation. Millennials have been proficient at looking inward, discovering the unique intersection between their passions and their marketability, and then charging full steam ahead towards the opportunity of achieving their very own brand of creative, commercial and emotional fulfillment.

Ironically, one of the most influential forces behind our self-centred methodology is the very same source that holds a great deal of power to inspire (or worse, impose) a reversal and unleash in us a gravitational pull towards a much more conservative centre: our parents.

For every part self-indulgence we have stored as their privileged children, they have stored two parts pride as our trailblazing parents; assistance has never been in their plans, but we’d be pushing our independent spirit a bit too far if we didn’t pause for a moment and consider a place for it in ours.

I don’t mean that in a, “Get your head out of your ass and get ready for the geezer apocalypse” kind of way. I just mean that in a, “Let’s give this even 5% of the thought we give to our Instagram feeds” kind of way. Let’s just take a moment to know where we stand, financially and ideologically.

If your parents are stinking rich and you have the utmost confidence that behind the scenes all their books are balanced, congratulations; you have been blessed with the genetic luxury of walking away from this article without the need for concern or calculator. For the rest of us, we may want to run some numbers.

According to a federal finance report, Canadian Millennials are “the wealthiest they’ve ever been” – front-end Millennials (born in the former half of the 80s) apparently have an average net worth of $93,000. That number might be a tad misleading in the broader context though – that’s just a snapshot of aggregate value, liquid and non-liquid.

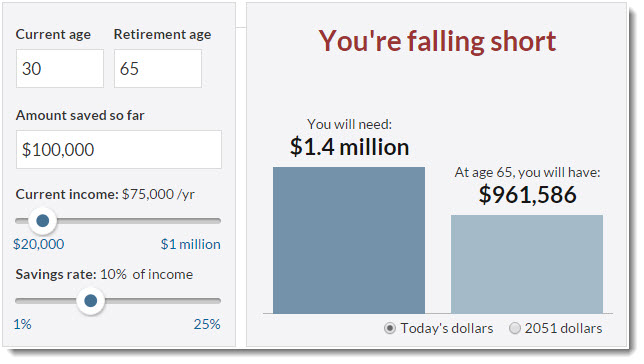

A study from Environics Analytics estimates that the average annual household income for Millennials in 2015 was $71,000. Using this nifty Retirement Calculator from CNN Money, you can get a rough idea of what your path to personal retirement looks like, adjusting variables like age and percentage of income saved:

Assuming $100K in savings, $75K in annual income and a 10% savings rate, a 30-year-old looking to retire at 65 will be almost half a million dollars short of what they’ll likely need for a comfortable retirement – that accounts for the current age averages, where 65-year-old men tend to live until 84 and 65-year-old women tend to live until 87.

If you look at reports from sources like BMO or the Employee Benefit Research Institute, that kind of discrepancy won’t shock you; Baby Boomers are falling an average of $400K short of their savings goals, with the average retirement savings for people 55-74 at about $180,000.

If you’re wondering about CPP, under the current model, that pays out a max of about $12,000 per year.

Taking it a step further. Let’s imagine that at around the age of 80 the topic of living in a “retirement home” hits the table. In Toronto, for example, the lower-end facilities will run you about $2,500 to $4,000 per month. Getting all fancy and opting in for nicer accommodations and even perhaps a kitchen, you’re looking at upwards of $6,500 per month. Of course things like having pills delivered and engaging in supervised activities outside the grounds are extra. Some facilities also only include two meals a day in their base price.

I think you’re getting the idea; life gets more expensive, and if we keep our heads down, we could quickly be facing a significant amount of debt because there’s no “P” in YOLO.

Much like my prior article, this is not meant to be a scare tactic, a guilt trip, or a discouragement from zeroing in on your dreams and doing your best to make them a reality. I don’t know what kind of loans you’ve taken out from The Ancestral Bank of Canada, but it’s not like you technically owe your parents anything… aside from perhaps a bit of consideration for where their lives are headed and how, if at all, you factor in that future from the newly minted position of bread-winner.

When I speak to most Millennials, they haven’t really given this much thought. Their mentality seems to be one of, “I assume they’ll be fine – plus, it was kind of their responsibility to make sure they were prepared.” I agree, which is why it’s important to acknowledge that responsibility sooner rather than later. It’s not like you can just pivot to print money, but at the very least you can make decisions about your career and your lifestyle with a balanced sense of outbound accountability. Or if not with a sense of balance, at least an honest, explicit commitment to indifference.

Many parents of Millennials who are stable and set for retirement are in that position because more than 30 years ago they made considerations just like these. We shouldn’t feel like we have shoes to fill, but we’d be wise to follow in a few sensible footsteps. I’m worried that in a relentless pursuit of self-satisfaction and personal legacy, many of us are forgetting to do up our laces.

[ad_bb1]